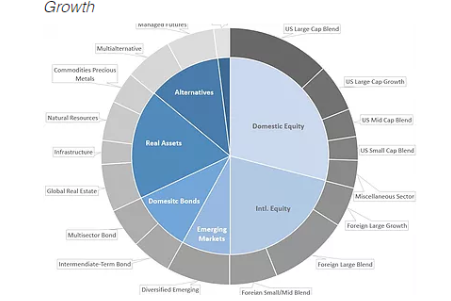

Strategic Portfolios

Our portfolios begin with creating strategic asset allocations for the Growth and Income Portfolios. The strategic allocations for each portfolio have different risk/return profiles. All portfolios are well diversified and designed to meet different investment objectives.

Strategic Asset Allocation can be thought of as the baseline long-term asset allocation for each portfolio.

Asset Allocation Process

The first step in our Asset Allocation Process is to establish a strategic (long-term) asset allocation for each portfolio. We believe that at the core of building a diversified and efficient portfolio is Modern Portfolio Theory (MPT).

According to the MPT, it's possible to construct an "efficient frontier" of optimal portfolios. We utilize the expected return, correlations, and standard deviation of various asset classes to design the most efficient growth and income portfolio.

Building Blocks

The first step is to determine the type of asset classes and investments to use in constructing the portfolio. Below is a list of some asset classes.

These broad asset classes can be further broken down into sub asset classes that can be used to create a more efficient portfolio. For example, international stocks would include developed markets and emerging market equities as well as growth and value components.

Asset allocation and diversification do not assure or guarantee better performance and cannot eliminate the risk of investment loss. As with any investment strategy, there is the possibility of profitability as well as loss.